As we entered 2026, the backdrop for investors looked broadly supportive. Inflation had moderated from its post-pandemic highs, interest rates appeared close to their peak, and the global economy continued to demonstrate surprising resilience, helped by a fresh wave of corporate investment in artificial intelligence (AI) infrastructure.

For a time, this looked like the continuation of a comfortable trend, with growing confidence that central banks could guide inflation back to target without triggering a slowdown.

Then came March. The conflict in the Middle East triggered a significant energy shock. The closure of the Strait of Hormuz, causing disruption to the global supply of oil and other critical commodities, pushed prices higher forcing a rapid repricing across financial markets.[1] Equities fell, bond yields rose and investors were left to reassess the consequences of a prolonged conflict.

Yet, as so often during periods of geopolitical stress, markets ultimately proved willing to see past the immediate shock. As the second quarter progressed, investors increasingly concluded the conflict would be contained and that the spike in oil prices would prove temporary.[2] Following the announcement of a ceasefire framework, that assessment appeared broadly correct. Equity markets recovered strongly and, by the end of June, many risk assets had regained their losses and moved on to fresh highs, despite the longer term resolution of tensions in the region remaining uncertain.

Inflation strikes back

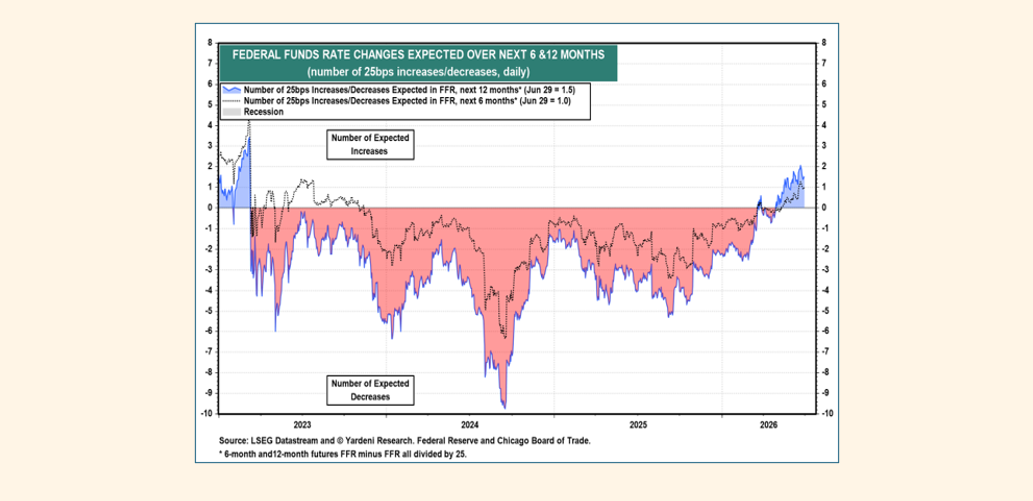

For much of the last three years, investors had operated within a relatively familiar framework: inflation was expected to fall steadily, central banks would eventually cut interest rates, and declining bond yields would provide a supportive backdrop for both equities and bonds. As 2026 has progressed, that assumption has begun to be challenged.

In many ways, this marks the first meaningful change in momentum investors have faced since inflation peaked in 2023. For several years, markets were largely debating when interest rates would begin to fall. Today, the conversation has shifted towards whether they may need to rise further.