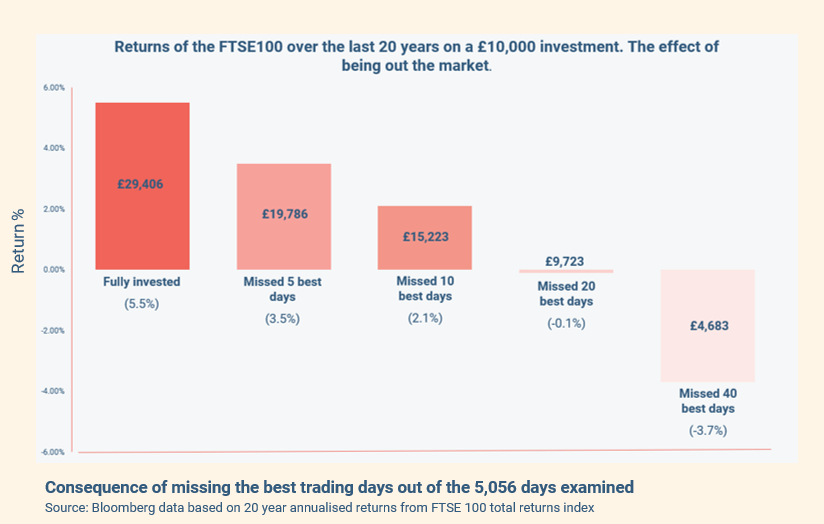

An all-too-common issue in the UK is our attachment to having cash in the bank. This is a problem that was exacerbated by the COVID pandemic as spending decreased and stock market volatility returned. In fact, household savings reached their highest level since formal records began in 1987. “That’s not a problem?!” I can hear you thinking… “we’re all getting wealthier and are building up our cash reserves – great!”. Unfortunately, the opposite could be the reality. As our levels of cash build, we are effectively accumulating an ever-depleting asset and losing ‘money’ at a rate of knots. The belief that cash always brings security is generally founded on misinformation. As such, many of us either have misconceived ideas as to what to do with our cash or suffer from severe apathy and simply let it build. Maybe cash isn’t king after all…

Understanding the cash in your bank account

The Consumer Price Index (CPI) is the primary measure of inflation the Government uses. To determine the rate, they create a ‘basket’ consisting of 720 goods and services that is designed to represent what the average person regularly spends their money on. They then take the average price of all the items and assess how this price changes. In 2019, for example, CPI was 1.3%. Assuming the interest on your current account is non-existent, (like mine!) this meant that in 2020, the cash in your bank account would buy 1.3% less of the goods in the basket. The purchasing power of your money literally falls year on year. The Bank of England even targets a 2% inflation rate, so it’s a fairly consistent pattern of depreciation too.

However, the CPI basket is rarely representative of what you personally spend your money on. Unless, of course, you find yourself regularly puffing on cigars, reaching for your windsurfing board, carrying a bag of coal, or putting together your adult jigsaw puzzle… yes, all of those were in the 2020 basket of goods! Sounds like one wild weekend. Jokes aside, it highlights an important reality – CPI is an arbitrary measure, based on an average, so will rarely be applicable to your own circumstances. It should be considered a very rough guide, at best.

Your personal inflation rate

To truly understand how inflation impacts you, you need to calculate your ‘personal inflation rate’. You can dive into ONS figures and online data to determine this but there are also various personal inflation rate calculators available online. I recently gave this a go myself and analysed six months of my credit card and bank statements to calculate my own personal inflation rate. Interestingly, my rate was a whopping 3.69%. This is far higher than the current CPI figure, and my spending patterns aren’t particularly unusual or lavish. Whilst I was slightly shocked, this is an extremely common finding. Rarely will an individual’s personal inflation rate sit at the same level as CPI. For high-net-worth individuals, it can creep much higher than mine – check out the Forbes ‘cost of living extremely well index’ that has averaged north of 5% since it began in 1982.

What does this mean? Well, with a personal inflation rate of 3.69%, if I had £500,000 and left it in a bank account for just 3 years, with interest at the average base rate, I would suffer a loss in real terms of £49,392. That’s almost £1,400 a month! Even if I sourced the highest interest rate savings account available, I would still lose £41,445. If you were watching that money fly out of your bank account, you’d be utterly horrified. However, simply because the number stays the same on our screens, we don’t give it any real consideration when trying to make informed decisions about our money.