Feeling the squeeze? You’re not alone. More and more people are facing the same challenge – balancing their own retirement needs while financially supporting both ageing parents and adult children. For some, this means making tough choices and sacrifices; for others, it’s about managing significant wealth and understanding complex tax rules.

Whatever your situation, the common thread is this: With the right planning and financial advice, it’s possible to manage these competing demands without compromising your financial security.

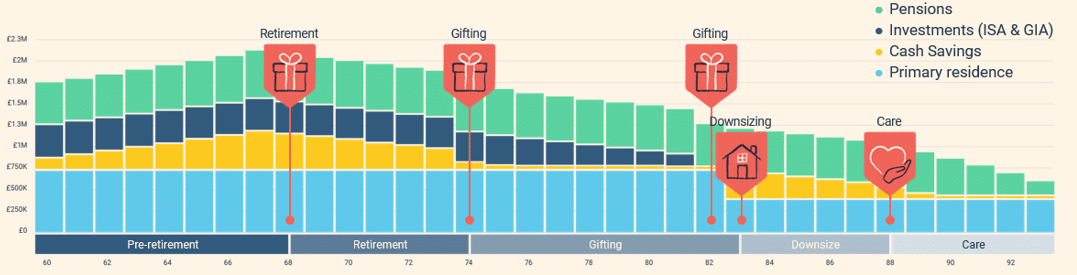

Understanding the UK sandwich generation

Coined in 1981 by social worker Dorothy Miller, the term ‘sandwich generation’ describes those supporting aging parents and adult children – often without receiving reciprocal support themselves.[1] With longer life expectancies, rising care costs, and adult children staying financially dependent for longer, the result is a growing financial squeeze. According to the Office for National Statistics (ONS), almost 1.4 million people in the UK fall into this category.[2] Reports indicate that balancing these dual responsibilities can be particularly taxing on mental health, with many experiencing heightened stress and emotional strain. Given these challenges, seeking professional financial advice can often be helpful in clarifying priorities and support long term resilience for both the individual and their family.

Our latest Saltus Wealth Index (September 2025), a biannual survey of more than 2,000 people with over £250,000 in investable assets, tracks the financial confidence, attitudes, and priorities of the UK’s affluent. It reveals that 76% of high net worth individuals are providing financial support to adult children (18 and over), 42% to grandchildren and 56% to ageing parents or grandparents. A notable 22% are supporting both children and parents at once.[3]