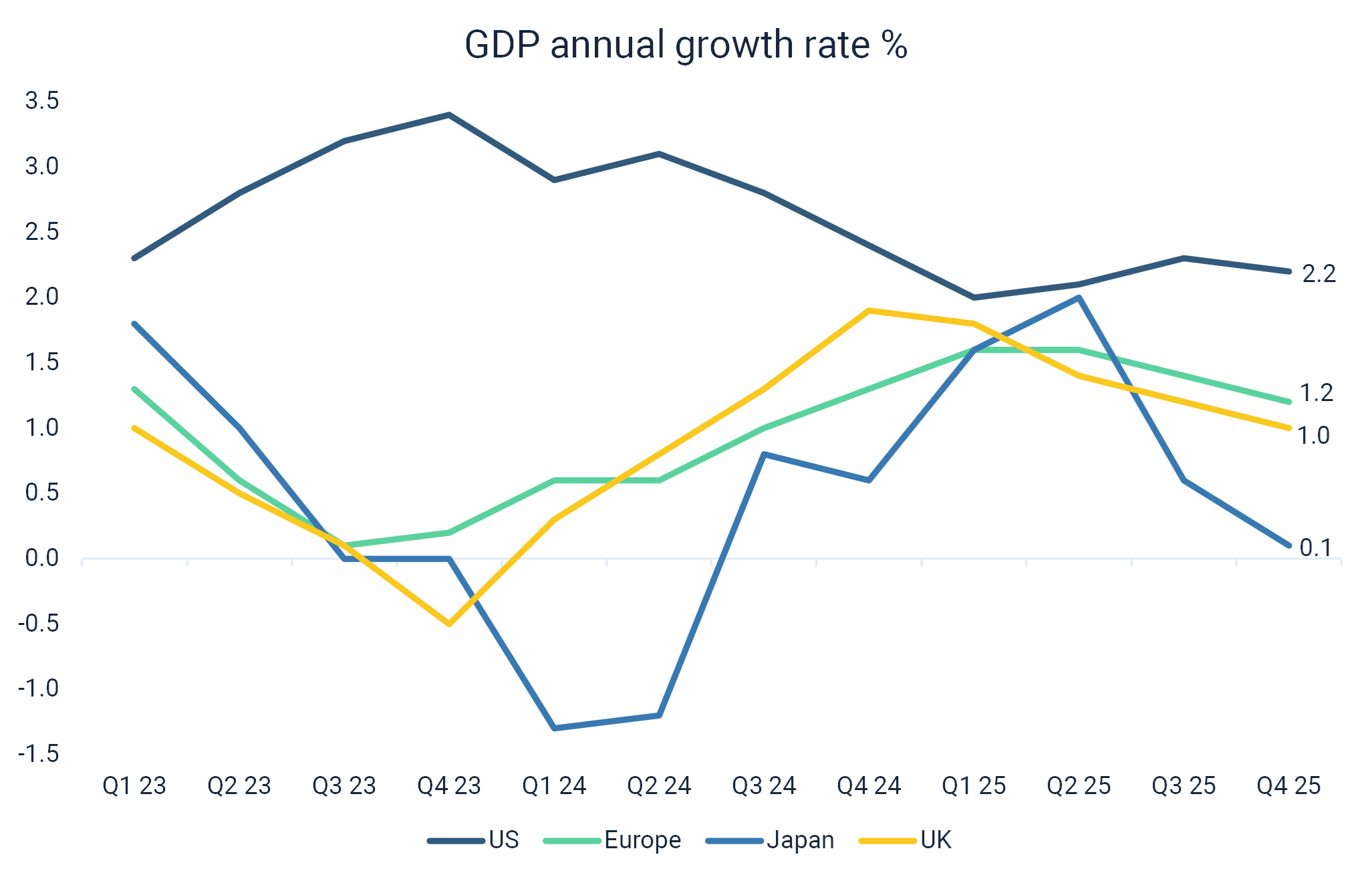

Broad economic growth eased towards the end of 2025, although it remains at healthy levels with positive momentum. The outlook remains for growth in 2026 to be at or above trend, supported primarily by continued strength in the United States. The US economy is still benefitting from vast amounts of AI capital expenditure, falling interest rates and low unemployment, which could help offset the geopolitical turbulence emanating from the US.[1] A prolonged oil price rise could reduce economic growth through 2026 if we see significant supply disruptions.[2] Europe, UK and Japan are more exposed to rising energy prices as they are large energy importers.

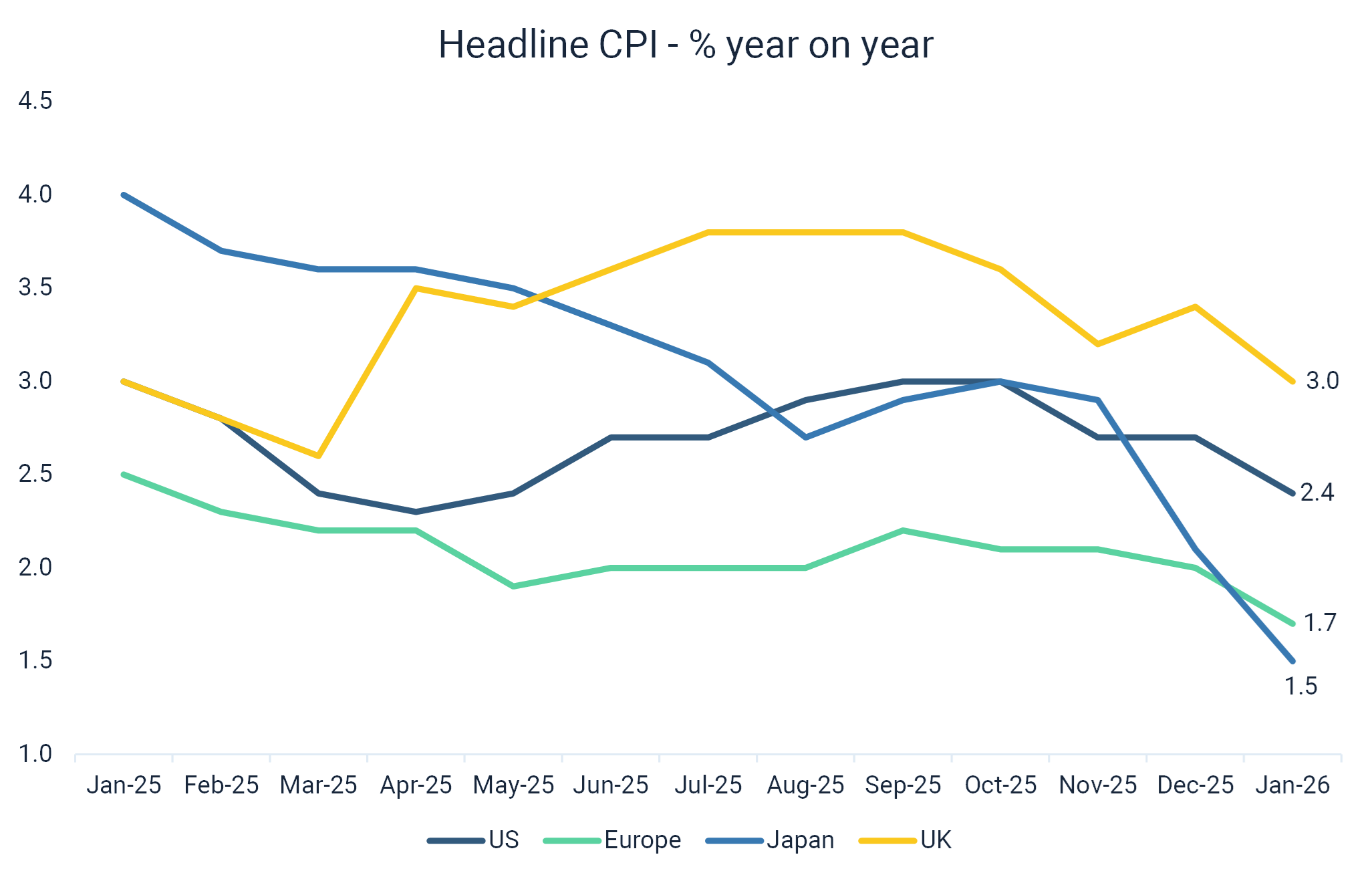

Inflation continues to fall and is now almost in line with central bank targets. The exception to this is in the UK, where inflation, even though it has fallen, is still significantly above the Bank of England’s target. [3] The increase in US tariffs has not had a meaningful impact on inflation in the US, however, a prolonged oil price shock could cause inflation in all regions to start picking back up, akin to 2022 when Russia invaded Ukraine.