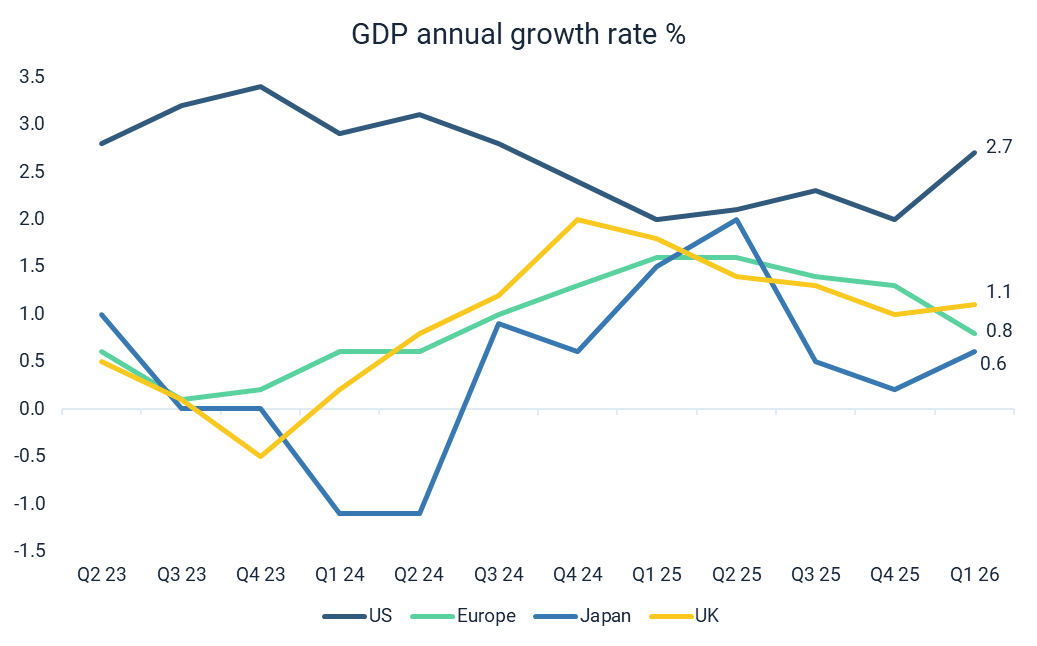

Global economic growth has continued on a slowly decelerating path in 2026 so far. The slight cooling is primarily driven by recent geopolitical disruptions, notably the conflict in the Middle East, which has strained energy supply chains and dampened earlier economic momentum.[1] Major economies exhibited diverging growth trajectories. The UK showed unexpected resilience and was the fastest growing economy in the G7 in Q1. This was largely driven by a strong services sector. The US saw a modest expansion, again driven by AI and technology investment. The Eurozone, Japan and China economies were relatively subdued.

Investment conditions

Source: Saltus, Trading Economics

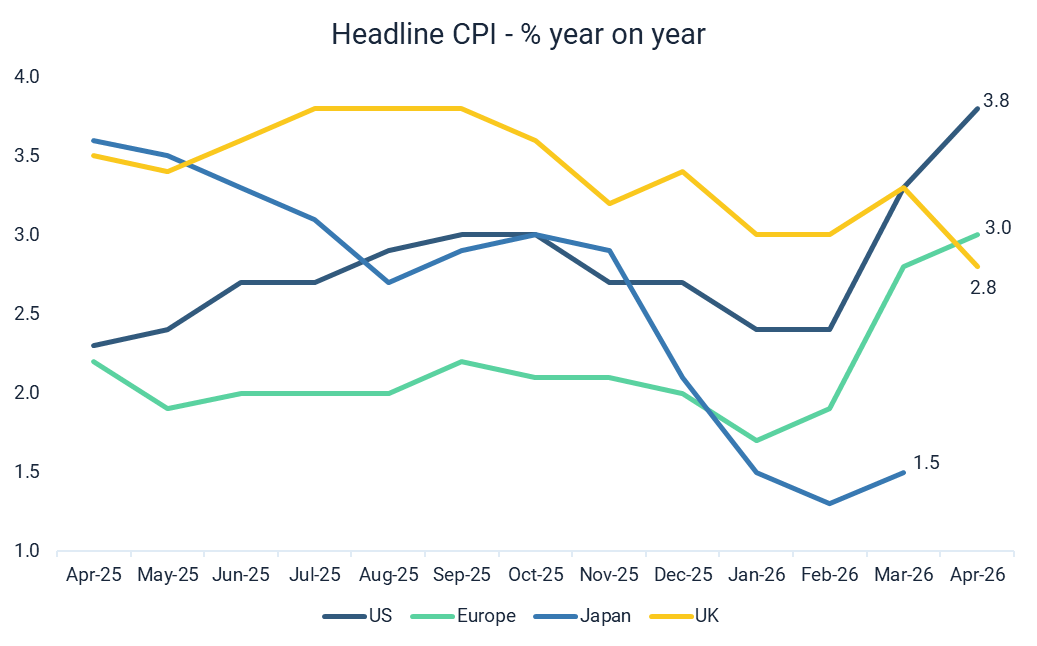

Global inflation has ticked up meaningfully over the last few months due to a surge in energy prices and broader commodity prices, as a direct result of the conflict in the Middle East. In the US, inflation is now at its highest level since May 2023.[2] Europe followed the same trajectory. The UK is something of an outlier, with inflation actually falling, helped by price resets at the start of the fiscal year and a downward contribution from housing and the energy price cap.[3] The Bank of England expects inflation to pick back up in the months ahead though. Japan is experiencing more moderate inflation, even though it is a big importer of energy.

Source: Saltus, Trading Economics

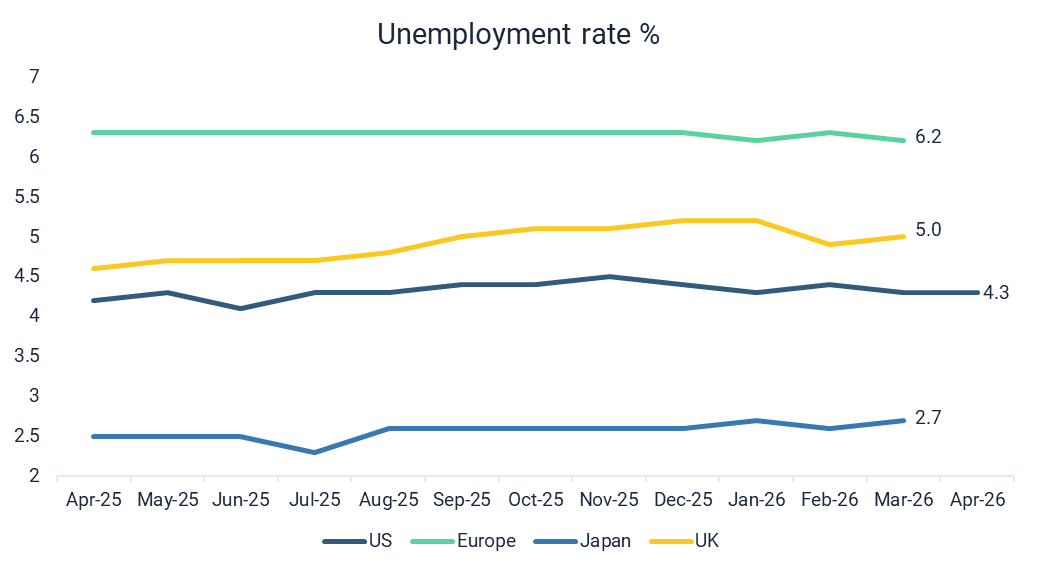

The labour market across the four major economies has experienced gradual loosening over the last few months, though all unemployment rates remain low by historical standards. There are signs of deterioration in the UK labour market, which was softening even before the Middle East conflict broke out. Japan is still experiencing near full employment.

Source: Saltus, Trading Economics

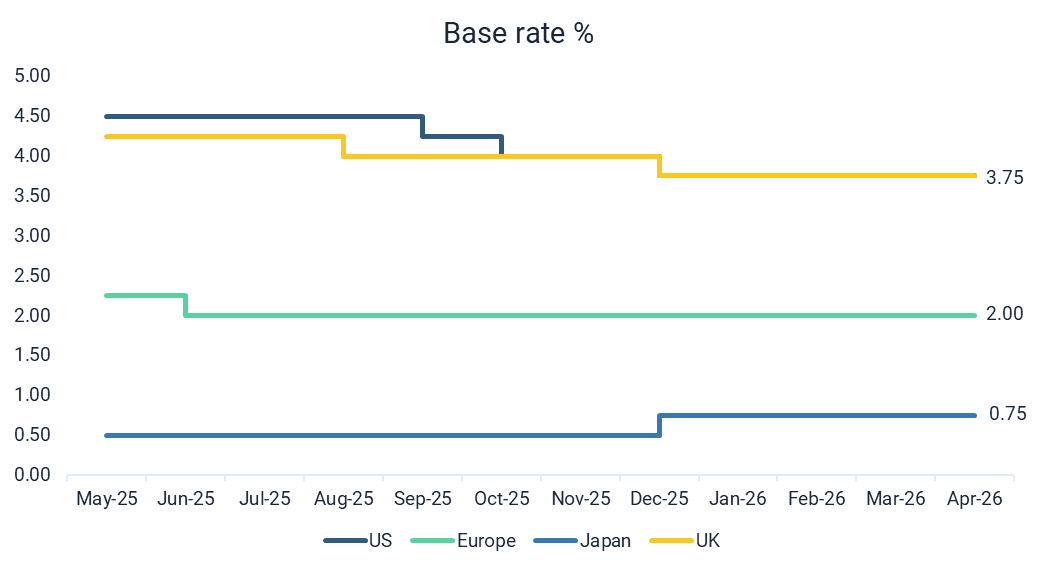

There were no notable interest rate changes in the last two months. Rising inflation expectations caused by a spike in the oil price have caused markets to reduce their expectation of any further rate cuts in the US and UK this year. The Bank of Japan are expected to continue hiking, albeit slowly, and the European Central Bank could hike rates towards the end of 2026. The cutting cycle could be over for now.

Source: Saltus, Trading Economics

The 2026 first quarter earnings season has proved to be one of the strongest in recent memory, with results materially exceeding the cautious expectations that prevailed at the start of the reporting period. In the US, with 91% of S&P 500 companies reporting, 84% have delivered a positive EPS surprise and 80% a positive revenue surprise, and the blended year-on-year earnings growth rate has reached 27.7%, up sharply from the 13.1% expected at the end of March (Source: FactSet). Margins have been a particular highlight, with the blended net profit margin at 14.7%, the highest since FactSet began tracking the metric in 2009.

The picture in Europe has been considerably more muted but still better than feared. STOXX 600 companies were forecast to deliver Q1 earnings growth of around 4%, reversing the 2% year-on-year decline recorded in the previous quarter, with energy sector profits surging roughly 25% on Middle East-driven oil prices, though stripping out the energy windfall leaves the rest of the STOXX 600 with just 1.5% earnings growth on average, barely above stagnation.[4] Two cross-cutting themes have dominated commentary on earnings calls: geopolitical risk and the Iran energy shock, which has displaced tariffs as the dominant macro concern, and continued strength in AI-related capex and revenues, which has anchored the technology-led leadership of the US results. Importantly, since most Q1 business activity predated the late-February outbreak of hostilities, the headline numbers offer only limited insight into the true cost impact. The bigger test will come in Q2, when margins will be squeezed by higher energy and input costs against a backdrop of softening consumer demand.

Market Themes

Below are a couple of other interesting market themes.

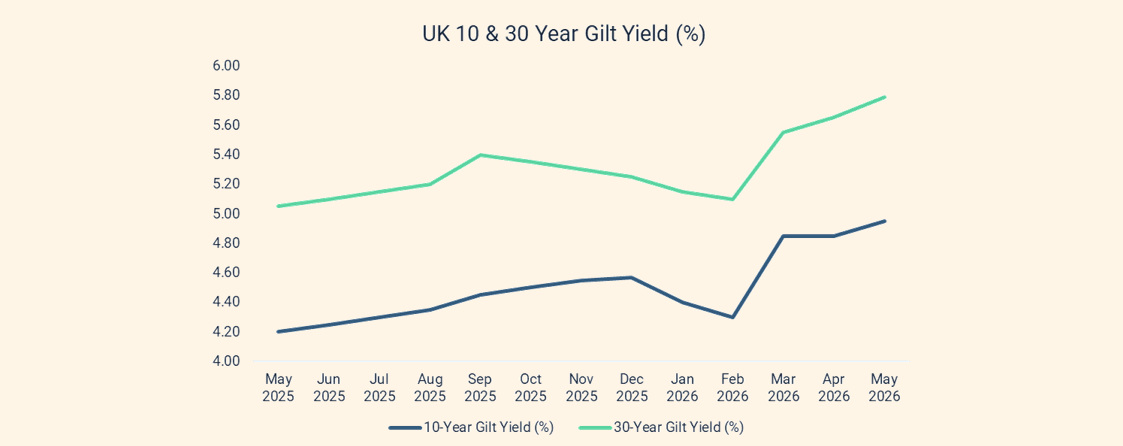

The repricing: How gilt markets turned

UK government bond (gilt) yields have moved sharply higher over recent weeks, with the market caught between two powerful forces: international inflation pressures and growing domestic political uncertainty.

The catalyst has been geopolitical. The 10-year gilt yield climbed above 5% at one point in May, as hopes of de-escalation between the US and Iran faded. The 30-year gilt yield reached its highest level in almost 30 years. Whilst this has been a global phenomenon, the UK’s heavy reliance on imported energy has amplified its vulnerability to supply shocks, leaving gilts among the weaker performers in global bond markets.

Domestic politics have added a second leg to the sell-off. UK government bond yields have soared amid growing questions about who will lead Britain’s government and the future direction of fiscal policy, after the ruling Labour Party suffered significant losses in local elections earlier in the month. Investors are now focused on whether the government will embrace a more expansionary fiscal stance, as the deficit reduction program has been an important anchor for gilt investors.

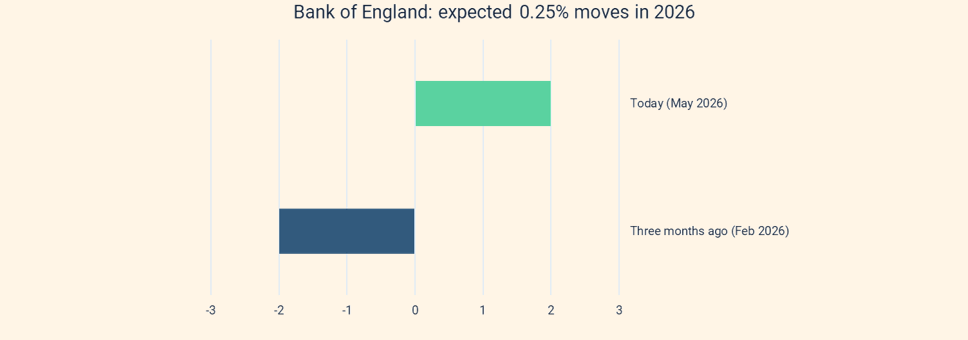

Rate expectations have flipped accordingly. Markets are now pricing in multiple Bank of England rate hikes this year, a stark reversal from pre-conflict expectations of two cuts.

Source: Saltus, Bank of England, UK – Implied Policy Rate Curve from Interest Rate Futures | UK Market | Collection | MacroMicro

The gulf shock goes global

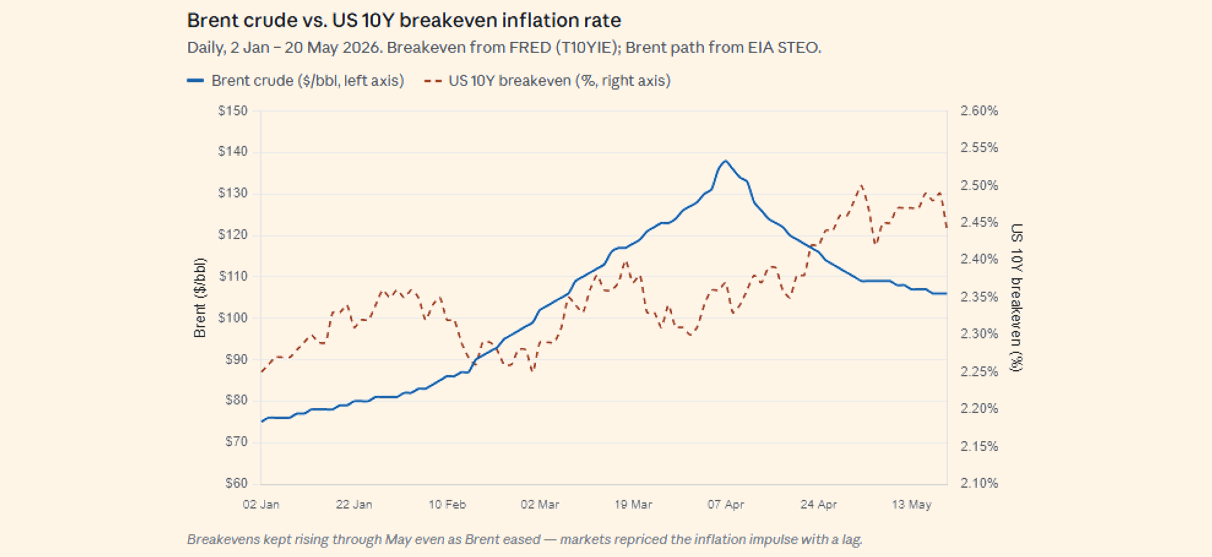

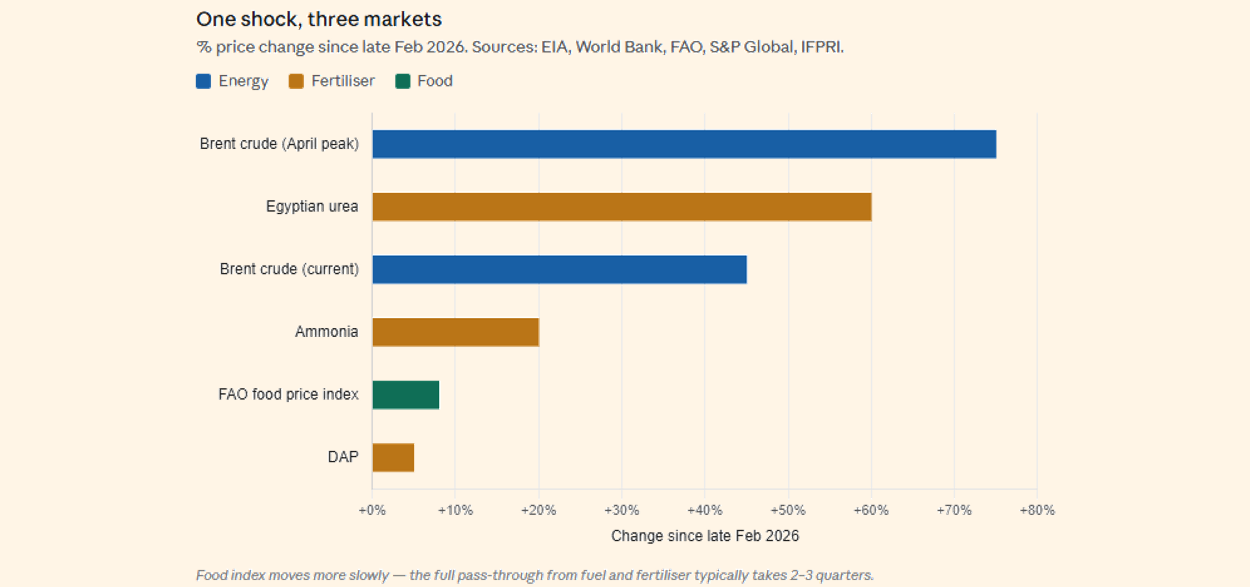

The conflict in the Middle East has triggered what the International Energy Agency (IEA) describes as the biggest energy crisis in history. With the Strait of Hormuz effectively closed, major Gulf producers have shut in a substantial share of global crude output, and Brent peaked at $138 per barrel in early April before settling above $100.[5] The US Energy Information Administration (EIA) expects prices to ease only gradually as flows resume later this year.

The shock is rippling well beyond fuel. Natural gas — the feedstock for nitrogen fertilisers — has surged, and Qatar has halted downstream urea production. The World Bank now projects fertiliser prices to rise 31% in 2026, with the Food and Agriculture Organisation (FAO) warning of reduced yields for fertiliser-intensive crops such as wheat, rice and maize if disruption persists.[6] Food inflation, which had only just begun to abate, is firming again.

The market response has been instructive. Through Brent’s climb to $138, the US 10Y breakeven rate (inflation expectation) rose only modestly, from 2.25% to around 2.37% — markets initially treated the oil spike as transitory. The real repricing came after Brent peaked, with inflation expectations reaching 2.50% in early May as the second-round effects through fertiliser, food and freight became clearer. In other words, markets are no longer pricing this as just an oil shock; they’re pricing a broader, stickier inflation impulse.

This shifts the rates outlook materially. Central banks that had pivoted toward easing are now likely to hold for longer, lifting real yields and weighing on rate-sensitive equities. Defensive sectors, energy producers and selected agricultural-input names are outperforming, while Emerging Markets (EM) consumer staples and import-dependent economies face the sharpest pressure.

Energy, fertiliser and food are moving as one linked complex, and the inflation path has shifted higher and later than markets first assumed. Expect elevated cross-asset volatility through year-end.

Views by asset class

Equities

The committee decided to maintain the current regional equity exposures. Around half our equity exposure is in the US, which we consider to be underweight given the US dominance in the global stock market. The other half of our equity exposure is spread broadly, with notable positions in emerging and frontier markets, as well as Japan.

Within our US exposure, for the last two years we have purposefully sought to diversify away from the technology sector given valuation concerns, concentration concerns, and too much dependence on the AI narrative. At the recent meeting, the committee decided to increase our allocation to US equities, reducing the degree of underweight; however, the portfolio continues to remain underweight overall. On the one hand, the US stock market is trading near record highs, and valuations are reaching historically elevated levels, but on the other hand, corporate earnings are the strongest of any region and the US economy is still the most productive and technologically advanced. We recognise both of these things, and our current US/non-US balance reflects this.

The committee also decided to alter the composition of our emerging and frontier market exposure. We are selling our direct Indian equity position. This is a relatively new position in portfolios, as we were confident that after a long period of underperformance relative to other emerging markets, there were structural changes taking place to attract investors back to the asset class. The Middle East conflict has changed this, as India is heavily dependent on oil from the Gulf, and so will be one of the hardest hit from the energy shock. We are still positive on the longer term prospects for the region, but there are better investment opportunities elsewhere for now. We are investing the proceeds from this sale into our existing emerging market exposures.

Our positions in UK, Europe and Japan are remaining broadly unchanged.

Bond

Within our fixed income exposure, we currently do not have a meaningful position in government bonds due to concerns around lingering inflation, fewer rate cuts, and the debt burden of developed economies. Where we do have government bond exposure, this is predominantly in UK gilts with a small holding in US inflation-linked bonds. We are maintaining a low level of interest-rate sensitivity, which has helped portfolios recently given rising bond yields. The committee decided to increase our exposure to US inflation-linked bonds, as these should provide additional protection against any energy-led spike in inflation.

Within corporate bonds, we had exposure to both investment grade and high yield debt. Given the high valuation of investment grade bonds, or the narrow yield spread above government bonds, most of the returns in this asset class derive from the government bond yield element. Given we are wary of government bond exposure, the committee decided to reduce our investment grade bond holding.

The proceeds from both of these sales will be held in cash for now. This allows us to be opportunistic should we identify attractive investments in either bond markets, or other parts of the portfolio.

Alternatives and Currency

The committee decided to initiate a position in a commodity index. This gives portfolios broad exposure to a range of different commodities, including energy, agricultural products, industrial metals and precious metals. In a portfolio context, this position is in place to protect against an escalation of the current Middle East situation, with a prolonged closure of the Strait of Hormuz, and commodity prices staying elevated as a result. As we saw in 2022, both equities and bonds can struggle in this scenario, and commodities are one of the few assets that could benefit.

We analyse our alternatives exposures across four different themes.

- Risk-off exposure – these positions should benefit from an increase in market volatility, especially on the downside. This includes traditional safe haven assets.

- Absolute return strategies – these strategies aim to achieve positive returns regardless of market direction.

- Alternative credit strategies – these target alternative parts of the credit market which have a low correlation to the wider market. These can include catastrophe bonds, trade finance and convertible bonds.

- Risk-on exposure – these positions should benefit from a strong economy and rising markets but provide an uncorrelated source of return. This includes the new position in the commodities index.

The committee are comfortable with our weighting across the four themes.

In currencies, we remain overweight Japanese yen and Emerging Market currencies, and underweight the US dollar.

Summary of positioning

Below is a summary of our views for each asset class, from strongly negative (- -) to strongly positive (+ +).

Asset Class

| Asset class | -- | - | Neutral | + | ++ |

|---|---|---|---|---|---|

| Equities | X | ||||

| Government bonds | X | ||||

| Corporate bonds | X | ||||

| Alternatives | X | ||||

| Cash | X |

Asset Class Breakdown

| -- | - | Neutral | + | ++ | ||

|---|---|---|---|---|---|---|

| Equities | USA | X | ||||

| UK | X | |||||

| Europe | X | |||||

| Japan | X | |||||

| Asia ex-Japan | X | |||||

| Emerging markets | X | |||||

| Bonds | US Government | X | Non-US Government | X | ||

| Inflation-Linked Government | X | |||||

| Investment Grade Corporate | X | |||||

| High Yield Corporate | X | |||||

| Emerging Market Debt | X | |||||

| Alternatives | Commodities | X | ||||

| Gold & Gold Miners | X | |||||

| Property | X | |||||

| Global Macro | X | |||||

| Equity Long/Short | X | |||||

| Absolute Return | X | |||||

| Infrastructure | X | |||||

| Currency | Sterling | X | ||||

| US Dollar | X | |||||

| Euro | X | |||||

| Japanese Yen | X | |||||

| Emerging Markets | X |

Fund in focus: Polen Capital US Small Company Growth Fund

Fund objective & philosophy

The Polen Capital US Small Company Growth Fund invests in smaller US companies that the manager believes can grow strongly over time. These companies are often earlier in their development than large, well-known businesses, which means they can offer attractive long term growth potential. However, they can also be more volatile, so careful stock selection is important.

The fund is managed with a long term mindset. Rather than simply buying the cheapest companies, the team looks for businesses that can increase their sales and profits over time. Their view is that, over the long run, share prices tend to follow the growth of a company’s profits.

The team focuses on three key ideas:

- Find companies that can grow strongly

The team looks for businesses with the potential to grow faster than the wider market. This could be because they have a strong product, operate in a growing industry, or are run by a high quality management team. - Spot important trends early

A key part of the process is identifying long term trends before they become widely recognised. Current areas of focus include the rising demand for electricity, artificial intelligence infrastructure, aerospace, defence-related technology, genomics and biotechnology. - Stay disciplined

Smaller companies can move sharply in value. The team therefore combines company research with valuation discipline and risk controls. In simple terms, they want to own exciting growth companies, but not at any price and not without understanding the risks.

Investment personnel & strategy

The fund is led by Andrew Cupps, who has managed this US small company growth strategy since it began in November 2000. He has more than 30 years of investment experience and has spent most of his career focused on smaller US growth companies.

Andrew is supported by a very experienced team. Kevin Leitner has worked on the strategy since its launch, while Chris Bush has been involved since 2007. This long-standing team is one of the fund’s key strengths. They have worked together through many different market environments, including recessions, periods of rising interest rates, and sharp market sell-offs.

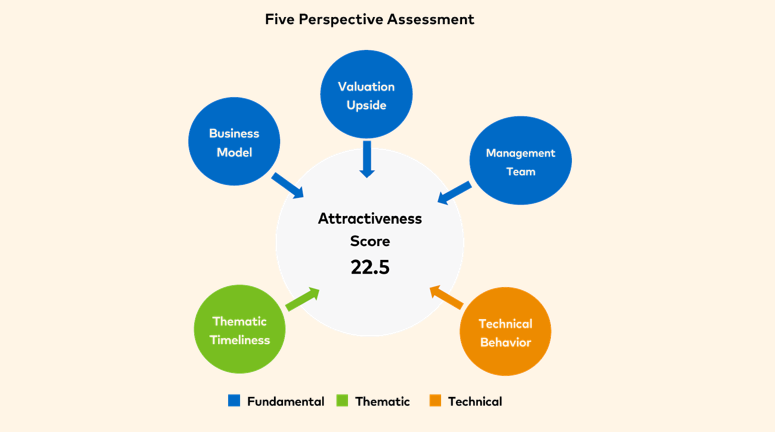

The team uses a structured process to decide which companies should be included in the fund. They assess each potential investment across five areas:

- Is the company linked to an attractive long term trend?

- Does it have a strong business model?

- Is the management team capable and trustworthy?

- Is the share price reasonable given the company’s growth potential?

- Is the share price behaviour supportive, or is the market warning them to be careful?

The team also uses a risk-management tool called the Balance Mechanism. This was introduced in 2017 after a period when the fund had too much exposure to one particular type of company. Its purpose is to stop the portfolio becoming too dependent on one theme, one style of investing, or one source of risk.

Role in client portfolios

We use the Polen Capital US Small Company Growth Fund to provide clients with exposure to a different part of the US equity market.

Many portfolios are heavily concentrated in large US companies, particularly the largest technology names. Polen focuses instead on smaller businesses across a broader range of industries, offering access to earlier-stage growth opportunities and helping to diversify overall US equity exposure.

The fund also stands out due to the experience and stability of the investment team. Andrew Cupps has managed the strategy for more than 25 years, supported by a long-standing team that has worked together through multiple market cycles. This consistency is particularly valuable in small cap investing, where outcomes are more driven by stock selection and manager judgement.

Sources:

Asset Allocation Committee

The committee consists of several senior members of the investment team, all partners, who invest their own money alongside clients. The committee consists of:

Article sources

Editorial policy

All authors have considerable industry expertise and specific knowledge on any given topic. All pieces are reviewed by an additional qualified financial specialist to ensure objectivity and accuracy to the best of our ability. All reviewer’s qualifications are from leading industry bodies. Where possible we use primary sources to support our work. These can include white papers, government sources and data, original reports and interviews or articles from other industry experts. We also reference research from other reputable financial planning and investment management firms where appropriate.

The views expressed in this article are those of the Saltus Asset Management team. These typically relate to the core Saltus portfolios. We aim to implement our views across all Saltus strategies, but we must work within each portfolio’s specific objectives and restrictions. This means our views can be implemented more comprehensively in some mandates than others. If your funds are not within a Saltus portfolio and you would like more information, please get in touch with your adviser. Saltus Asset Management is a trading name of Saltus Partners LLP which is authorised and regulated by the Financial Conduct Authority. Information is correct to the best of our understanding as at the date of publication. Nothing within this content is intended as, or can be relied upon, as financial advice. Capital is at risk. You may get back less than you invested. Tax rules may change and the value of tax reliefs depends on your individual circumstances.