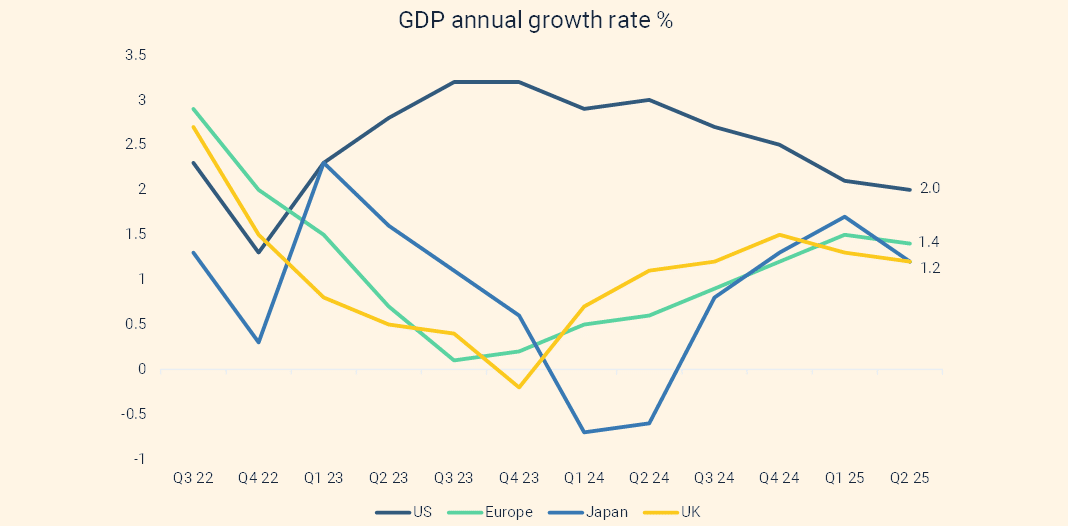

The major economies continue to see positive economic growth; however, growth rates are slowing. In the US, economic growth is back to trend levels and is widely expected to slow further from here as higher tariffs work their way through the system.[1] Cracks in the economy can already be seen in the US labour market. In the other major developed economies, growth rates are stalling, having recovered through 2024. Expectations are for a continuation of this trend – slowing GDP growth, but not to recessionary levels.

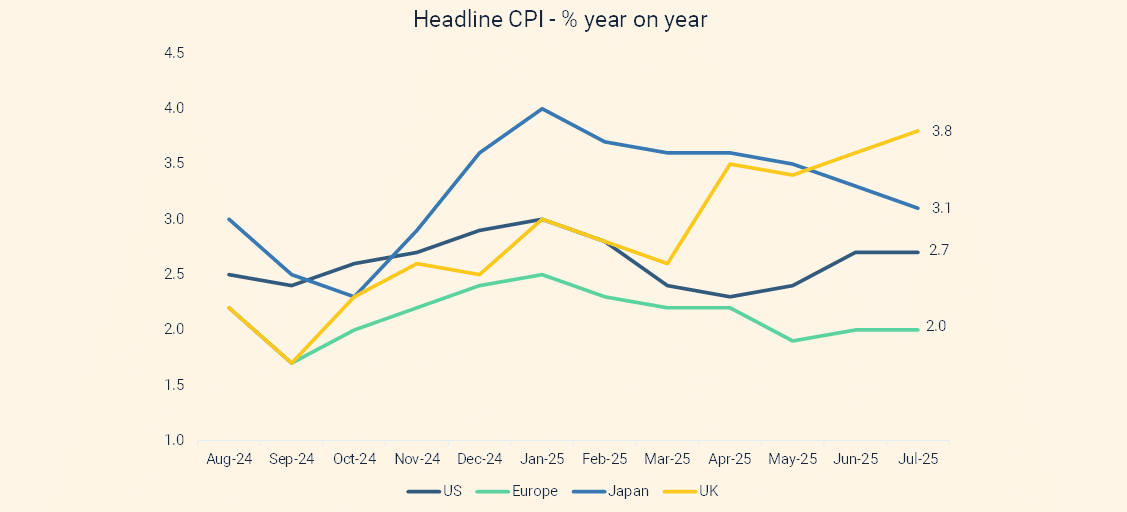

The picture is mixed on inflation. Headline CPI has been rising for the last four months in the US and is forecast to be over 3% by the end of 2025. Tariffs are expected to send inflation higher in the short term, but the impact should be temporary. The UK is also experiencing rising inflation. UK headline CPI is almost twice the Bank of England’s 2% target.[2] In Europe, inflation has been at or below target for the last 3 months but has the potential to start moving up again as we move towards the end of the year.[3] Japan has had a much needed reduction in inflation, and China is still battling with outright deflation.