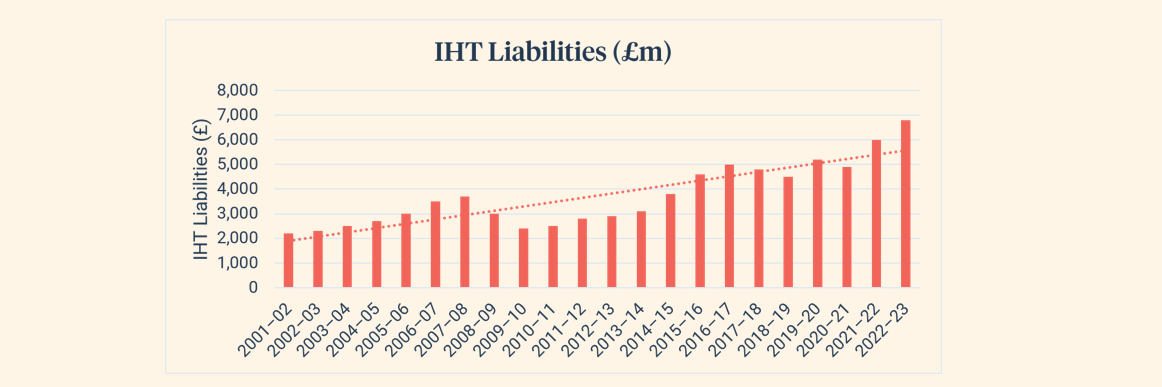

Inheritance tax (IHT) is affecting more families each year, and for many it is becoming an increasingly important part of estate planning conversations.[1] With inheritance tax thresholds frozen until at least the 2030 to 2031 tax year, and pensions set to be brought into the inheritance tax net from April 2027, estates that once sat comfortably below the limits are now being exposed to potential tax charges.

As a result, understanding the options available to reduce an inheritance tax bill is more relevant than ever. Gifting is a well-known approach, but one particularly valuable exemption can sometimes be overlooked. Known as the normal expenditure out of income exemption, or more commonly gifting out of surplus income, this relief can offer a practical and tax‑efficient way to pass wealth to loved ones during your lifetime, provided the rules are followed and the right evidence is kept.

Inheritance tax

Inheritance tax is charged at 40% on the value of an estate above certain tax‑free thresholds when someone dies. Everyone has a standard nil‑rate band of £325,000, which can be passed on without inheritance tax and is currently frozen until the end of the 2030 to 2031 tax year. In addition, there is the residence nil‑rate band, which can be worth up to £175,000 where a main home is left to direct descendants such as children or grandchildren. This means that, in many cases, up to £500,000 can be passed on free of inheritance tax.[2]