If you have come across the term ‘in-specie transfer’ and wondered whether it relates more to zoology than wealth management, you are not alone. The phrase can sound misleading at first glance, yet it describes an important decision point when moving investments from one wealth manager, or financial provider, to another. While both in-specie and cash transfers can be used to move investments to a new provider, they differ vastly in terms of complexity, costs, timelines and administrative demands.

In practice, a cash transfer is typically far simpler and faster than an in-specie transfer. That said, there are circumstances where an in‑specie transfer may be appropriate. Understanding how each works enables you to form clearer expectations around the process and choose the route that best supports your wider financial objectives.

What are in-specie transfers?

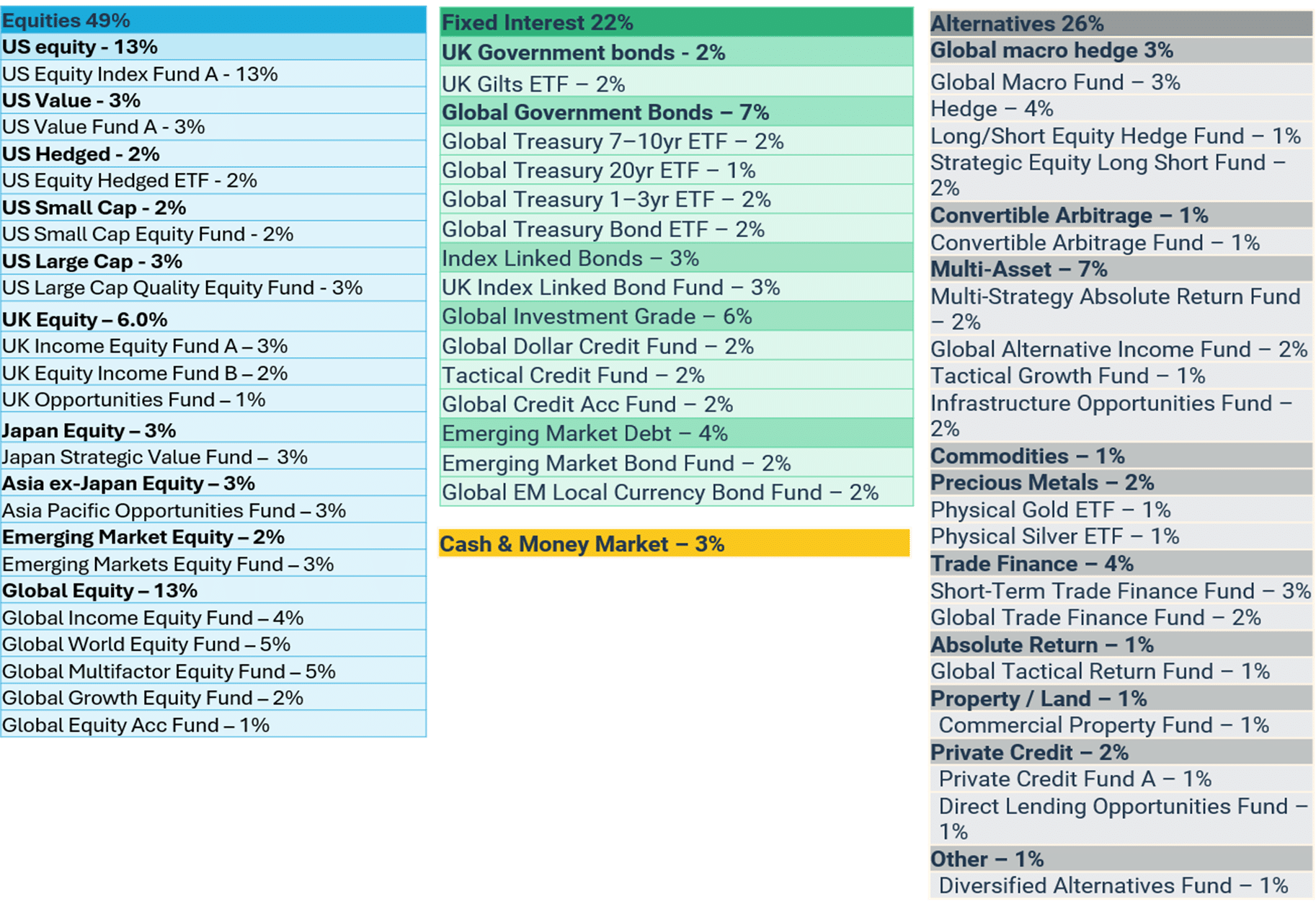

An in-specie transfer is the process of moving investments “as they are” from one provider to another without selling them first.[1] Rather than converting your holdings into cash and repurchasing them at the new platform, the assets remain invested throughout the transition. This process can include shares, funds, bonds, or other eligible securities.