Summary:

- More people will vote in 2024 than in any previous year

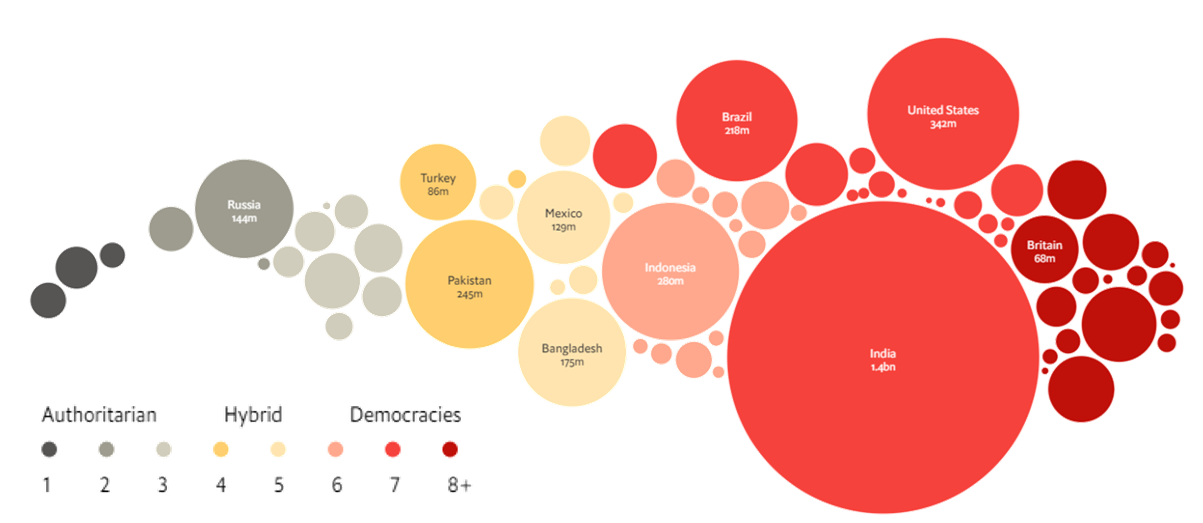

- In a period of heightened political uncertainty

- So elections will dominate the headlines

- But they won’t necessarily dominate financial markets or investment portfolios

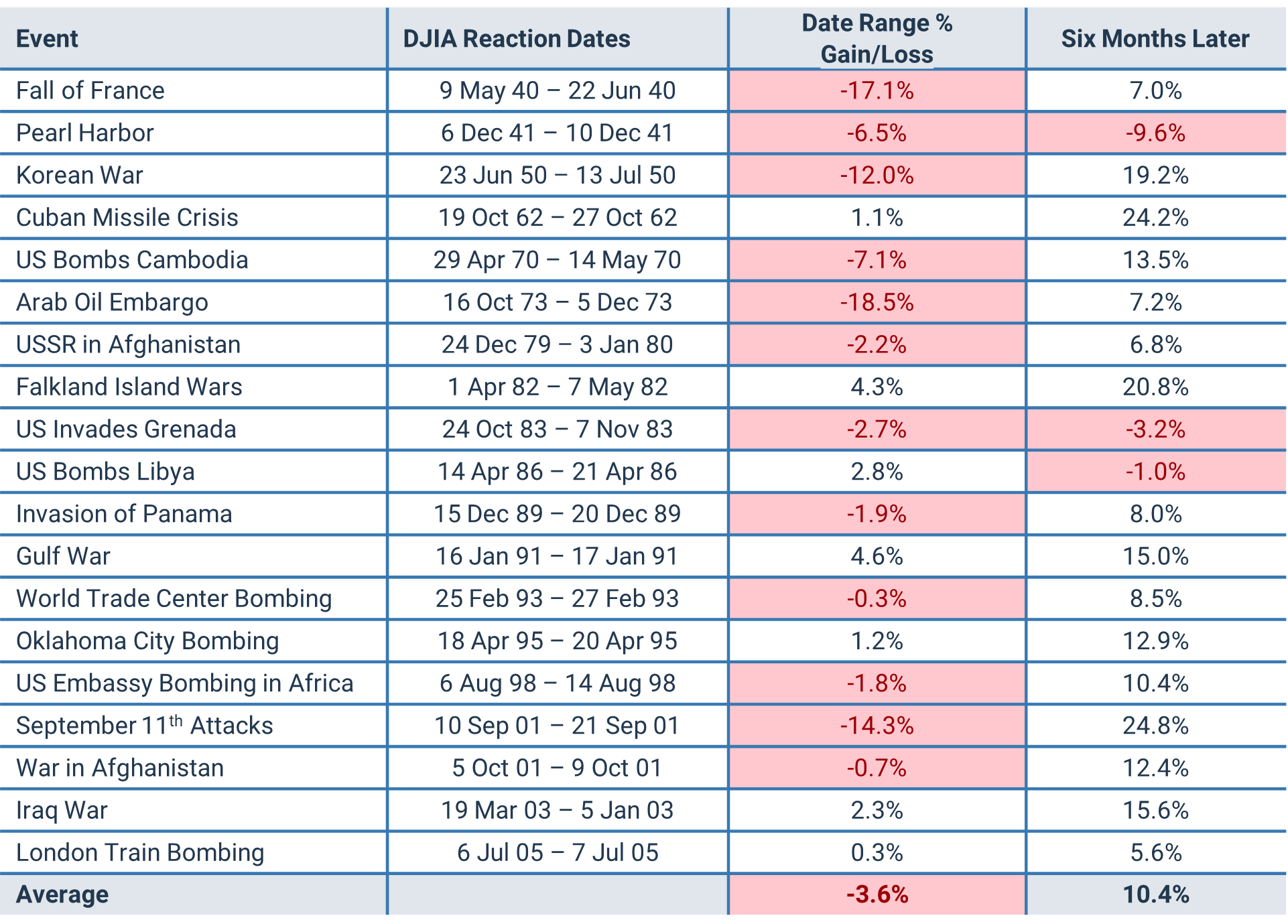

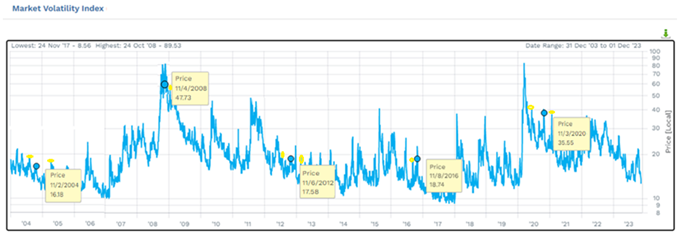

- Historically, elections have created volatility around the election date, they rarely change the direction of markets

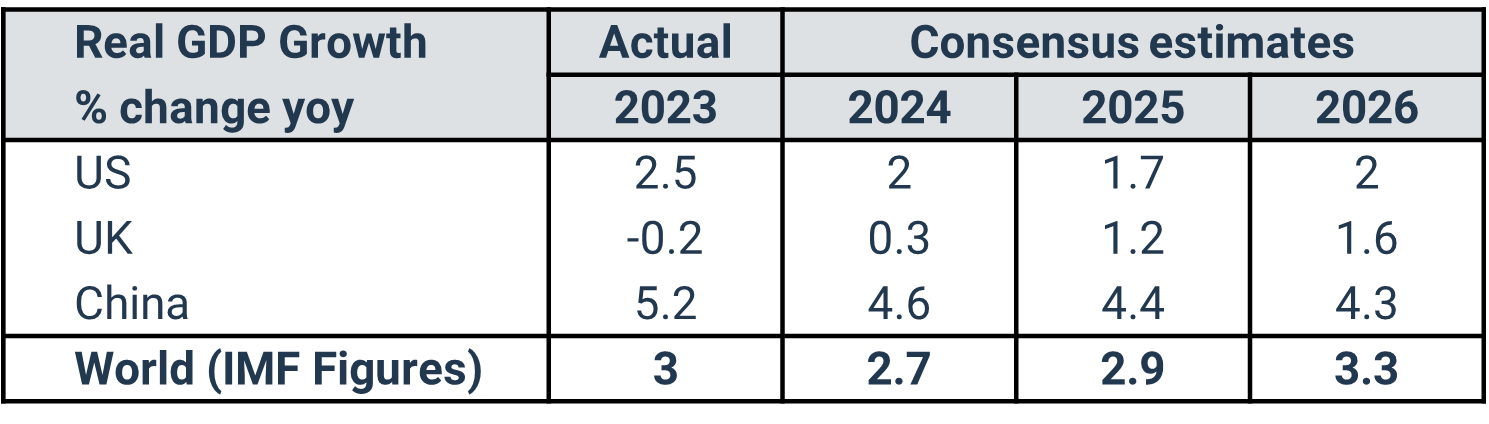

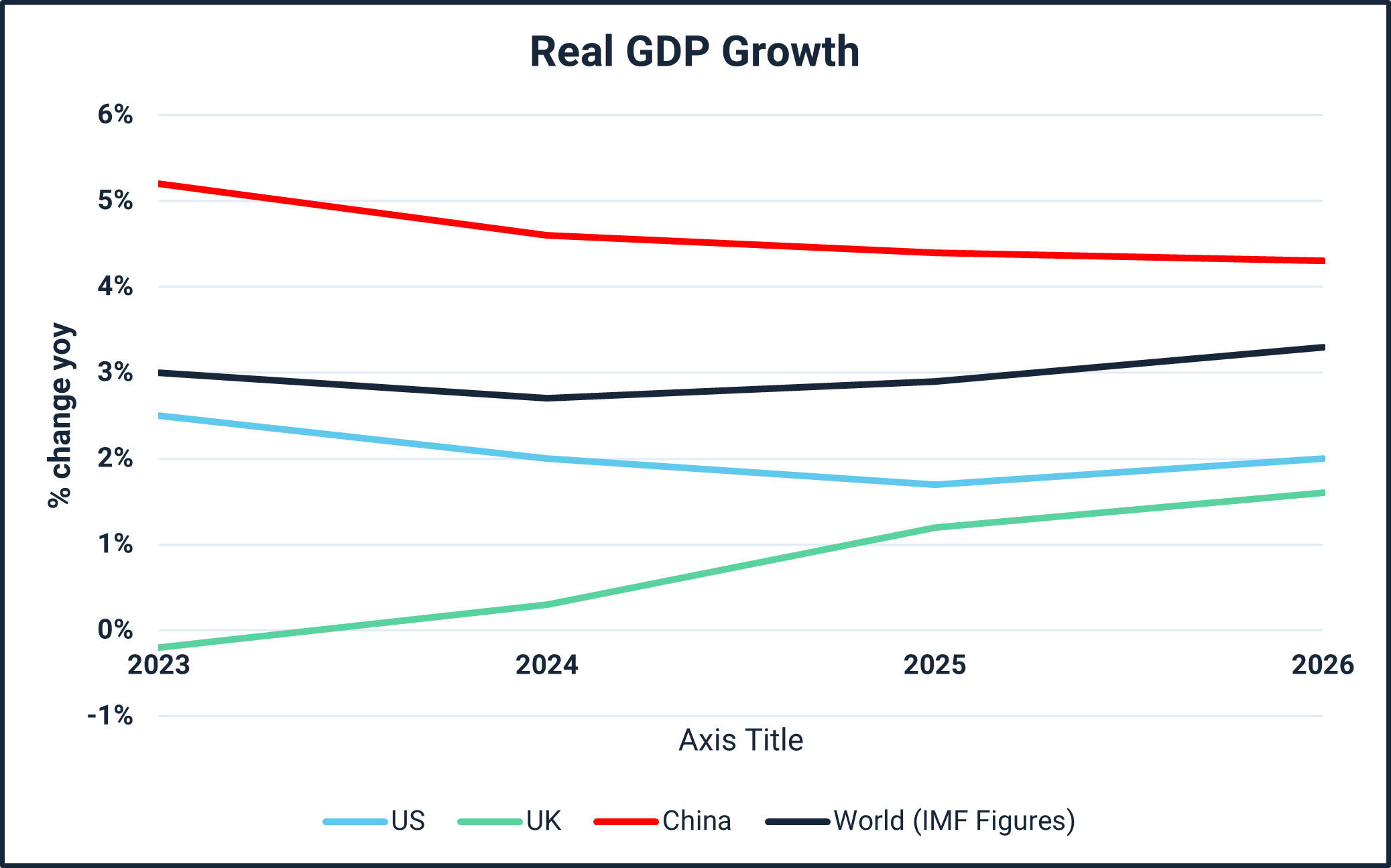

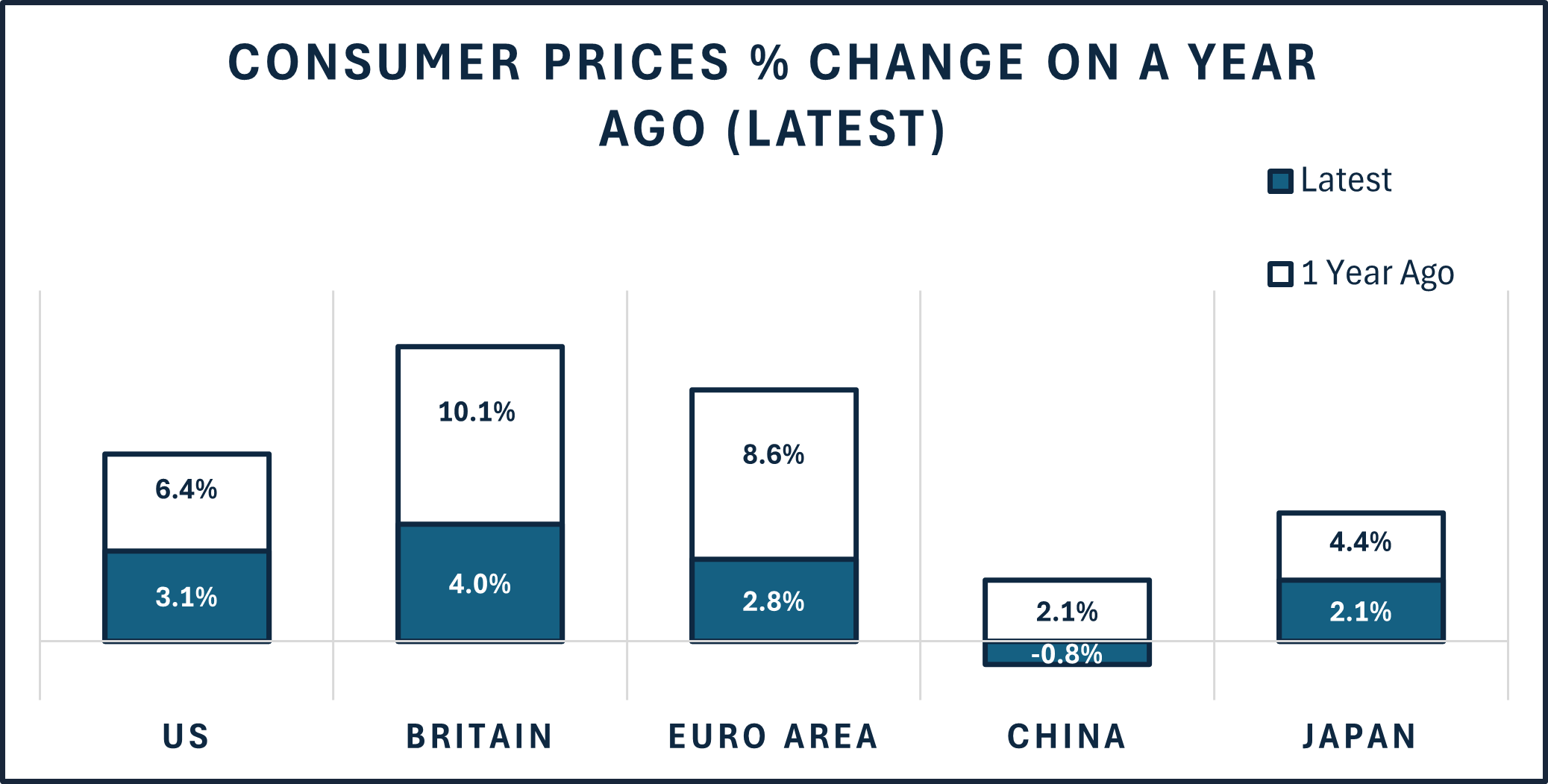

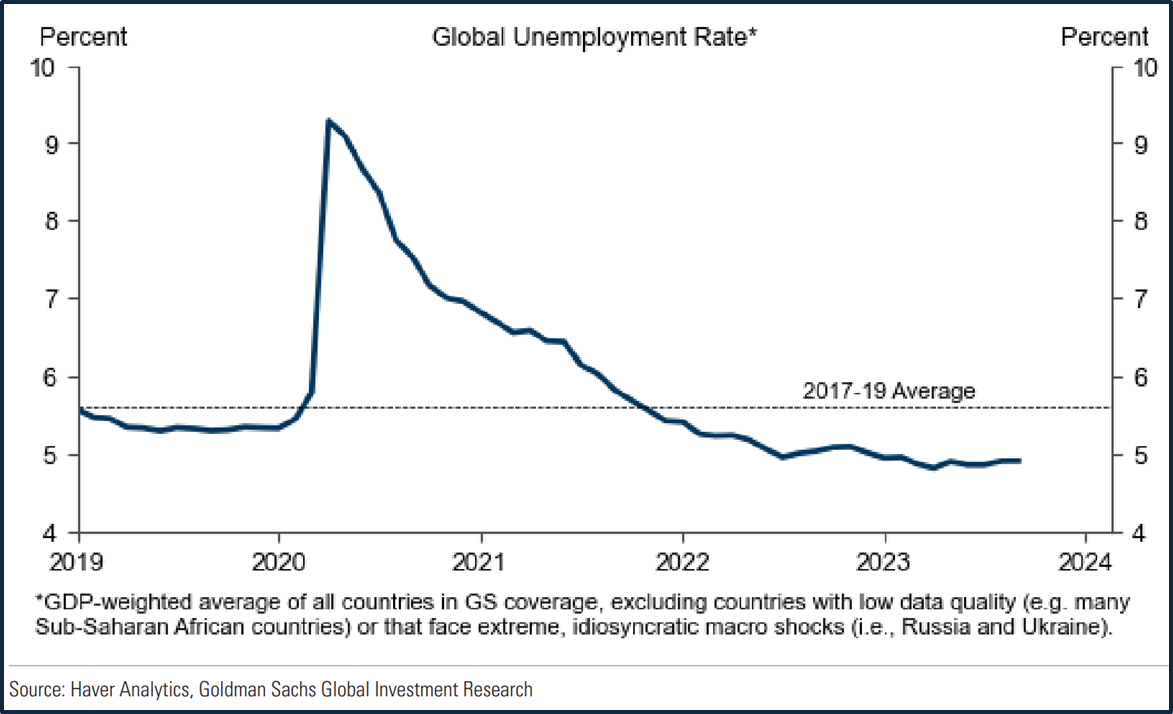

- Because markets are more impacted by economic variables such as growth, employment, interest rates, and currency movements, and politicians generally have limited impact on these (especially where there is an independent central bank like in the UK and USA)

- Saltus will be watching political developments closely, but we will focus on events that could affect our portfolios and do our best to block out the noise

We take comfort from the fact that Saltus portfolios are very widely diversified, we try and find many sources of return, that are each dependent on different factors, to reduce our reliance on individual companies, markets, asset classes, currencies, sectors… and politicians!